Collectively, Americans owe nearly $1 trillion on credit cards.

Total credit card debt stood at $986 billion at the start of 2023, unchanged from the record hit at the end of 2022, according to a new report on household debtfrom the Federal Reserve Bank of New York.

Typically, balances fall in the beginning of the year as borrowers start paying down debt after the peak holiday shopping season. “This is the first time in 20 years we are not seeing a decrease,” according to New York Fed researchers, citing inflation and a higher cost of living.

More from Personal Finance:

3 financial risk areas for consumers to watch

Americans are saving far less than normal

A recession may be coming — here’s how long it could last

Credit card balances are up almost 20% from a year ago, according to a separate quarterly credit industry insights reportfrom TransUnion.

The average balance rose to $5,733 over that same period, TransUnion found.

“As inflation rose to near 40-year-high levels, many consumers have used credit to help manage their budgets, leading to record- or near-record high balances,” said Michele Raneri, TransUnion’s vice president of U.S. research and consulting.

“Unfortunately, credit card debt is likely only to keep rising in the near future,” said Matt Schulz, chief credit analyst at LendingTree.

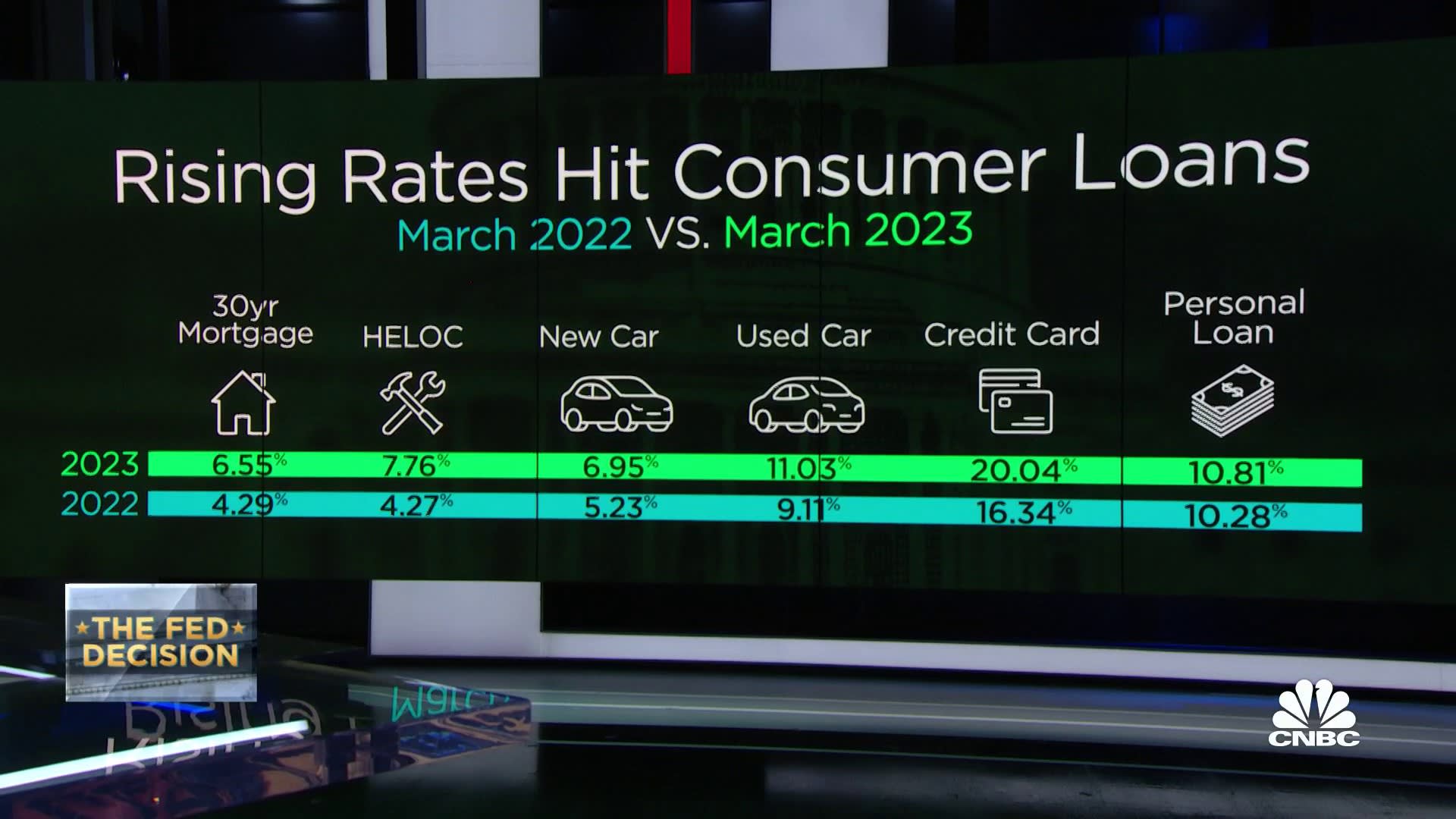

On the heels of another rate hike earlier this month by the Federal Reserve, the average credit card rate is now more than 20% on average, an all-time high.

Sky-high APRs make credit cards one of the most expensive ways to borrow money from month to month and yet, many Americans continue to take on ever-increasing amounts of debt. While balances are higher, nearly half of credit card holders carry credit card debt from month to month, according to a separate Bankrate report.

However, there are some strategies to help pay down high-interest credit cards once and for all. Here’s what experts recommend:

Five ways to tackle high-interest credit card debt

1. Reassess your spending. Most experts recommend starting with a basic budget. “The truth is that you cannot make a meaningful plan to tackle debt if you don’t know exactly how much money is coming in and going out of your household each month,” Schulz said.

“You may not like what you see, but it is better to deal with the reality of the situation than to bury your head in the sand.”

Getty Images

Using a worksheet or online tool can help you assess where you are spending money and how to better disperse those funds.

2. Plan a payoff strategy. There are two ways you could approach repayment: prioritize the highest-interest debt or pay off your debt from smallest to largest amount, according to Russell Nelson, manager of the credit card products acquisition team at Navy Federal Credit Union.

The avalanche method lists your debts from highest to lowest by interest rate. That way, you pay off the debts that rack up the most in interest first. The snowball method prioritizes your smallest debts first, regardless of interest rate, to help gain momentum as the debts are paid off.

With either strategy, you’ll make the minimum payments each month on all your debts and put any extra cash toward accelerating repayment on one debt of your choice. “You may also consider setting up automatic payments along with text alerts on your mobile device to ensure payments are made on time,” Nelson advised.

3. Snag a 0% balance transfer credit card. Cards offering up to 21 months with no interest on transferred balances are one of the best weapons Americans have in the battle against credit card debt, Schulz said.

Jroballo | Istock | Getty Images

To make the most of a balance transfer, aggressively pay down the balance during the introductory period. Otherwise, the remaining balance will have a new annual percentage rate applied to it, which is about 23%, on average, in line with the rates for new credit, according to Schulz.

4. Ask for a lower credit card rate. If you’re carrying a balance, try calling your card issuer to ask for a lower annual percentage rate. “You really have nothing to lose,” Schulz said.

In fact, 76% of people who asked for a lower interest rate on their credit card in the past year got one, according to a LendingTree report. You may also be able to get a reduced annual fee, higher credit limit or waived late fee, Schulz added.

5. Take advantage of high-yield savings accounts. In addition to paying down your debt, put aside some money to build up your emergency reserves, which will keep you from accumulating more debt while you’re working to pay off your existing balance.

“Robust savings are key to getting out of debt,” Schulz said.

Take advantage of competitive rates at an online bank, added Greg McBride, chief financial analyst at Bankrate.com. After years of rock-bottom returns, some top-yielding online savings accounts and one-year certificates of deposit rates are now as high as 5%.

“This could be ‘last call’ for savers,” McBride said, adding, “CD yields on maturities of one year and longer have peaked and now is the time to lock in.”