Ramsey Solutions financial expert Chris Hogan on how Americans can set a budget, tackle their debt and boost their retirement savings.

It’s not too late to start saving for retirement.

Continue Reading Below

Thirty-seven percent of all employees age 35 to 44, and 34 percent of employees age 45 to 54 have less than $1,000 saved for retirement, according to the Employee Benefits Research Institute.

Here’s how to start saving now

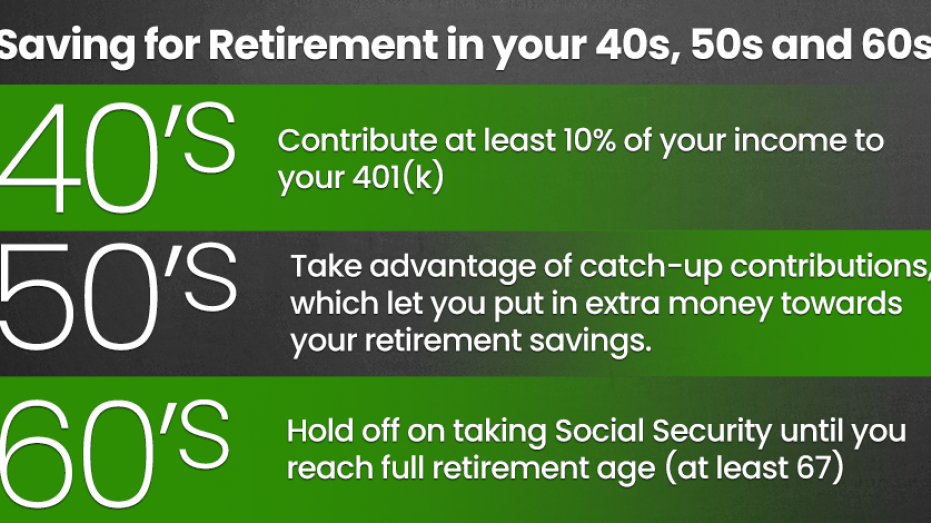

In your 40s:

Get your money to work for you. It’s still not too late to enroll in your company’s savings program. Most employers will offer a 401(k) option, and even match a portion of your investment. If they do, be sure to contribute the full amount. Many financial planners suggest contributing at least 10 percent of your income to a 401(k).

Take full advantage of your company’s savings plan in your 40s and contribute the max, financial experts suggest. (iStock)

Those who don’t have a company-sponsored savings plan can set up a traditional IRA (individual retirement account), which lets people contribute their pre-tax income toward investments. Another option is a Roth IRA, in which investments are funded with after-tax dollars and contributions are not tax deductible.

“Don’t let retirement savings be a casualty of your children’s education costs. Your kids can borrow money to go to college; you cannot borrow money to retire,” Greg McBride, a senior financial analyst at BankRate.com told FOX Business.

If you already have a 401(k) or another retirement plan in place, increase your contrubtion if it’s not already maxed out.

In your 50s:

It’s time to play catch up. Employees age 50 and up should take advantage of catch-up contributions, which let you put in extra money towards your retirement savings.

The catch-up contribution for a 401(k) is $3,000. The IRS limit on annual contributions to an IRA has been raised to $6,000 for 2019, up from $5,500 in 2018, and the catch-up contribution limit for people 50 and up remains $1,000, according to Investopedia.com.

In your 60s

The earliest you can start taking Social Security is at age 62, but experts advise against taking it too early. You can get more monthly income if you hold off on taking Social Security until you reach full retirement age, which is 67. If you’re married, having one spouse take Social Security early while the other prolongs it is also an option, retirement experts suggest.

It’s also important to review your investments.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

“As you are closing in on retirement make sure your retirement investments are allocated appropriately, given the fact that you may be on the retirement doorstep but are also looking at what could be a 30 or 35-year retirement period,” McBride said. He added, “You want to scale back the risk, but not too much because you are still going to need growth in the ensuing decades to preserve your buying power for the future.”